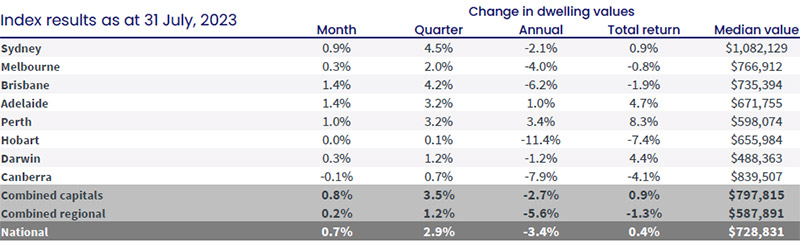

Property prices nationally rose 0.7 per cent in July, marking a fifth consecutive month of housing value recovery.

Adelaide and Perth were the standout property markets over the past month as real estate values nationally recorded a fifth consecutive month of increases.

CoreLogic’s national Home Value Index rose 0.7 per cent in July, as property prices continued to retrace the 9.1 per cent decline from the record highs of April 2022.

Nationally, prices are up 4.1 per cent since February but remain 5.3 per cent below the April 2022 peak. Only Perth, Adelaide and regional South Australia recorded a new cyclical high in dwelling values through July.

Regional values continued to lag behind the capitals, with the combined regionals index rising 0.2 per cent in July compared with a 0.8 per cent increase across the combined capitals index.

Every rest-of-state region recorded a smaller change in dwelling values through July relative to the capital city, reflecting milder housing demand across regional Australia as demographic patterns normalise.

Source: Corelogic.

CoreLogic Research Director, Tim Lawless, noted the most substantial reduction in growth has occurred in Sydney.

“After leading the upswing, the monthly pace of growth in Sydney housing values has halved from a recent high of 1.8 per cent in May to 0.9 per cent in July.

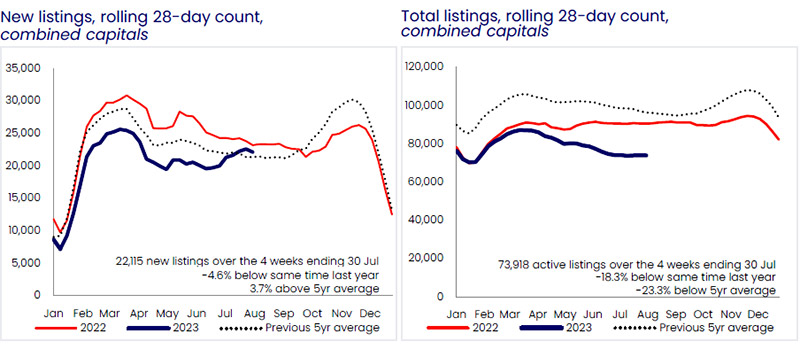

“Sydney has also seen a significant rise in the number of fresh listings added to the market, 9.9 per cent higher than the same time last year and 18.0 per cent above the previous five-year average.

“An increased flow of new listings provides more choice and may be working to reduce some of the urgency felt among prospective buyers,” he said.

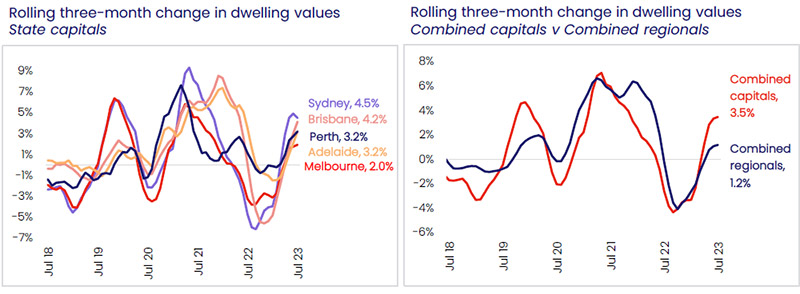

Brisbane and Adelaide saw the monthly pace of growth accelerate in July, leading the pace of gains across the capitals with housing values up 1.4 per cent across both cities.

Source: Corelogic.

Although the trend in new listings has risen in these cities, Mr Lawless said the number remains well below levels from a year ago and the previous five-year average.

Canberra was the only capital city to record a decline in values in July, down 0.1 per cent, while Hobart values were unchanged.

Market conditions, however, continue to be solid in the face of the low supply of sales listings around the nation.

Property Investment Professionals of Australia (PIPA) Chair, Nicola McDougall, said the significant price falls simply did not materialise in many property markets – even with the most rapid increase in interest rates in a generation.

“Of course, part of the reason why prices have been strengthening is the significant number of overseas migrants – some half a million – who have landed on our shores within the past year or two, which is also causing rental markets to continue to struggle with a critical undersupply of stock,” she said.

Source: Corelogic.

Ms McDougall said as well as healthy market conditions, it appeared that the rising interest rate cycle may have come to an end.

“The Reserve Bank of Australia took its foot off the throttle in early July and held the cash rate steady at 4.1 per cent, which provided some confidence to property buyers around the nation,” Ms McDougall said.

“The June quarter inflation reading also came in well under market expectations at six per cent and with it highly possible we are at, or near, the peak of the cash rate.”

Sydney property price growing slowing

Sydney was the only city where the flow of fresh stock to market was higher than a year ago (+9.9%).

“Despite rapid rate rises and the so-called mortgage cliff, the market has carved itself into three distinct categories – the affordable, below $1.5 million corridors; the above $1.5 million areas; and the regionals.

“The everchanging landscape and dynamics is influenced by various factors such as economic conditions like the end of fixed rates and the high level of inflation, government policies, buyer preferences and affordability.

“Compound that with a strong immigration factor, and we have a stabilisation of value despite the negative economic and affordability outlook.

“Selling agents that were expecting a whole raft of properties to hit the market, as they report fielding increasing calls for market appraisals, are still to bring these properties on the market.

“Owners struggle to rationalise selling their properties, as they cannot qualify for a new loan at the same or higher level under the current lending constraints, and renting is also a struggle, with a strong shortage in most areas,” he said.

Brisbane housing in limited supply

Meighan Wells, Founder, Property Pursuit Advisors, said supply in Brisbane was as low as she had seen in 20 years.

She said people have been flocking to Queensland over the past two and a half years and no one is leaving.

“Pre-Covid, population fluctuations were common – people would come, and people would go.

“One of the common reasons for departure was to seek higher paying job opportunities interstate or overseas but with the ability to secure well-paying corporate jobs that have work-from-home, or hybrid arrangements, the requirement to relocate away from the Sunshine State has disappeared.

“The challenge for quality established housing supply is that no-one is selling until they can buy something else but no-one is leaving so we now have a bottleneck of owners who won’t sell until they can buy but can’t find anything to buy until someone leaves, and no-one is leaving and around and around it goes.”

Perth has strongest rental conditions

The strongest rental conditions nationally continue to be seen across the unit sector, where rents were up 2.9 per cent over the three months to July nationally, compared with a 1.9 per cent rise in house rents. Across the capital city and rest-of-state regions, the unit markets of Perth (4.3 per cent), Melbourne (4.0 per cent) and Brisbane (3.8 per cent) stand out with the fastest rate of rental growth over the rolling quarter.

That lack of supply was particularly keenly felt in the rental market, where investors had sold up in the face of tighter rental regulations and higher interest rates.

“Interest still remains very high for homes around the $500 to $600 range, with enquiries in the hundreds for each property, although that is still fewer than six months ago.

“City apartments are continuing to rent really quickly with a high amount of enquires and rents are still increasing, although not as dramatically as the last quarter.”

Mr White said a large majority of applicants are still desperately looking for a home.

“We see behaviour that reflects this constantly at home opens and in applications.”

Article Q&A

Have Australian property prices recovered?

CoreLogic’s national Home Value Index rose 0.7 per cent in July, as property prices continued to retrace the 9.1 per cent decline from the record highs of April 2022.

Which are the best performing Australian property markets?

Adelaide and Perth were the standout property markets over the past month as real estate values nationally recorded a fifth consecutive month of increases in to the end of July 2023.

Are rents rising in Australia?

The strongest rental conditions national continue to be seen across the unit sector, where rents were up 2.9 per cent over the three months to July nationally, compared with a 1.9 per cent rise in house rents. Across the capital city and rest-of-state regions, the unit markets of Perth (4.3 per cent), Melbourne (4.0 per cent) and Brisbane (3.8 per cent) stand out with the fastest rate of rental growth over the rolling quarter.

From cutting years off the length of a mortgage to maximising rental income, these seven tips highlight how there is much more to a good property manager than collecting rent and doing property inspections.

If you’re one of the 2.2 million Australians who own an investment property, cash flow is the priority.

With an estimated 80 per cent of Australian property investors employing the services of a professional property manager, your property manager should be one of the key professionals who help improve your cash flow.

While most property investors look to their accountant to help improve the cash flow of their investment property, they often forget the value a professional property manager can bring to a property’s cash flow.

Here are seven strategies your property manager can implement to improve your cash flow:

1. Optimise rent disbursement frequency

Consider the benefits of more frequent rent disbursements.

While monthly payments are common with most property managers, switching to weekly disbursements can save you on interest costs, if you match your mortgage repayments accordingly.

For example: If you consider a loan amount of $500,000, with an interest rate of 6.6 per cent, paying principal and interest on a 30-year loan term, the savings can become obvious.

Swapping from monthly mortgage payments of $3213 to weekly mortgage payments of $803, the interest savings over the 30 years could be up to $163,730 (or reducing the loan term by six years, five months).

By aligning rent disbursements with your mortgage repayment schedule, you can effectively reduce interest expenses and improve your cash flow.

2. Maximise rental income

By staying informed about market trends and conducting regular rent reviews, property managers can ensure income is not left on the table.

Many places haves generated weekly rent increases of up to $200, highlighting the potential for significant income growth.

Property managers will, of course, be bound by any state’s legislation regarding rent increases.

3. Minimise vacancy periods

Vacant periods can have a significant impact on cash flow.

A property manager should manage lease renewals and minimise downtime between tenancies.

Furthermore, your property manager can implement targeted marketing campaigns and utilise online platforms to attract prospective tenants quickly, reducing vacancy periods and optimising your cash flow.

4. Reimbursing water consumption charge

Ensure that all allowable water consumption charges are passed on to tenants.

Whether your property is new or old, your property manager can implement systems to accurately track and bill tenants for water usage, helping to offset your expenses.

In some areas, strata title properties don’t issue individual property consumption information, and this can impact your ability to seek reimbursement of water consumption from your tenants.

5. Fair pricing from tradespeople

Qualified tradespeople are essential for maintaining your property, but their costs can vary.

Your property manager can leverage their network of trusted professionals to ensure fair pricing for maintenance and repairs, preventing overcharging and minimising expenses.

Additionally, your property manager can obtain multiple quotes for larger projects and negotiate favourable rates on your behalf, ensuring cost-effective maintenance solutions without compromising on quality.

6. Implement preventative maintenance programs

Proactive maintenance can prevent small issues from escalating into costly repairs.

By scheduling regular inspections and addressing maintenance issues promptly, your property manager can help you avoid unexpected expenses and preserve your property’s value.

Additionally, a property manager can develop customised maintenance schedules tailored to your property’s specific needs, addressing potential issues before they impact tenant satisfaction and annual rental yield.

7. Manage insurance claims efficiently

In the event of an insurance claim, your property manager should be experienced in managing these claims, which can facilitate a swift resolution.

Their expertise in property management and established relationships with insurers and local tradespeople can expedite the claims process, ensuring minimal disruption to cash flow.

Your property manager can document and report property damage promptly, liaise with insurance adjusters on your behalf, and oversee repairs to ensure timely completion and reimbursement. By efficiently managing insurance claims, your property manager can safeguard your investment and maintain uninterrupted cash flow.

Article Q&A

Should I use a property manager for my investment property?

A property manager can help optimise rental income, minimise expenses and ensure a steady stream of revenue, even slashing years off the duration of a mortgage by optimising rent disbursement frequency.

Property buyers and sellers alike stand to save potentially big dollars if they time their property purchase right in relation to the seasons.

When considering purchasing an investment property, seasonality is often forgotten as one of the important aspects to consider. Seasonal changes will have an impact on buyer and seller sentiment, which in turn influences property prices and the movement of the market. Understanding the seasonal patterns will help property investors to time their purchases and sales, capitalise on seasonal trends, and maximise their returns.

How does seasonality impact property markets?

Spring/summer

While the overall effect of seasonality will vary by region and state, general trends and patterns can be observed when comparing the cooler months to the warmer months.

During the spring and summer months, the Australian real estate markets tend to be more vibrant.

Warmer weather encourages more open house inspections, auctions, and overall property activities (like gardening and renovating).

The warmer weather and sunshine often influences buyers to be more positive and optimistic and generally willing to get out and explore open homes in a positive light, which can influence the overall sales price for the seller.

The longer daylight hours and favourable weather conditions means there might be more stock available for sale on the market, more open homes, and more sales via auction campaigns.

Investors should take note of this, because when there is more activity and positive buyer sentiment, this is likely to increase real estate prices, particularly as it gets closer to Christmas and some buyers start to feel a little desperate to get into a home before Christmas, which might push up prices.

Sellers will usually take advantage of this increased activity and market their properties more aggressively, hoping to attract higher bids across the spring and summer months.

Characteristics of spring/summer markets:

increased buyer activity and competition

sellers are more willing to list properties

more open house inspections and auctions.

Autumn/winter

Conversely, the cooler months across autumn and winter typically see a decline in market activity.

Colder temperatures and shorter days may deter potential buyers from attending open houses and auctions, especially if it is unusually rainy or cold.

Seller sentiment may also wane, leading to fewer property listings.

This slowdown can be more pronounced in regions with harsher winter climates, such as Victoria, while warmer areas like Queensland we expect to see less of an impact.

Now consider Victoria, with its colder and more variable winter climate, experiences a more noticeable seasonal effect.

Buyers might be less inclined to venture out, and sellers may prefer to wait until spring or summer to list their properties.

It is likely some of the colder towns may experience reduced market activity and some supply issues when it’s cold.

There is an exception though.

Think about the areas close to snowfields and snowy mountains that are buzzing with activity over the winter months and ski seasons.

We are likely to see more properties come onto the market, and more buyer activity because the properties will be shown off in their best light – with views over the snowcapped mountains or holiday homes listed for sale to show off how they are busy and booked over the winter months.

Sometimes visiting tourists love the location so much they start to investigate options to purchase a holiday home or even relocate if they love the area during their visit. There is more about this below.

Characteristics of autumn/winter markets:

decreased buyer activity and fewer open houses in most areas.

less motivation for sellers to list properties, unless in areas close to the snow.

potential for fewer auctions and slower market pace.

Other considerations

There are always going to be exceptions to these rules. This is just the overall impact that seasonality can have on property markets, so it is really important to understand the market you will be buying in as well as how the seasons will impact that area.

Think about the below considerations:

Queensland

Queensland is known for its generally warm climate. Because it experiences milder winters compared to southern states, the colder climates won’t have as large an impact on the property markets here.

Because of its warmer weather, winter does not significantly deter market dynamics and many people who live in the southern states might consider relocating to Queensland into coastal cities like Brisbane and the Gold Coast that experience more consistency in the property markets, even during winter.

Property prices don’t drop as much during the winter months in Queensland, as the weather remains conducive to outdoor inspections and tourism.

Strategic considerations for property investors

If you are investing in property it is important to understand these seasonal trends so you can make informed decisions.

Timing the market

Investors looking for better deals might consider purchasing during the winter months when demand is lower, potentially securing properties at reduced prices. Selling during the summer months can attract more buyers and potentially yield higher sale prices.

Region focus

In warmer regions like Queensland, investing can be more consistent year-round, reducing the need to heavily time the market.

In colder regions like Victoria, investors might find better opportunities by targeting winter purchases and summer sales.

Specialty investments

In ski resort areas, focusing on winter investments can be highly profitable due to the seasonal tourism boom.

Vacation homes and short-term rentals in these regions can provide substantial returns during the winter season.

Market adaptability

Staying informed about local market trends and climatic conditions can enhance investment outcomes. Whether investing in steady coastal markets or booming winter resort areas, a nuanced approach to seasonality can significantly enhance investment success.

Article Q&A

Do the seasons affect property sales?

While the overall effect of seasonality will vary by region and state, general trends and patterns can be observed when comparing the cooler months to the warmer months. During the spring and summer months, Australian real estate markets tend to be more vibrant.

A leading property management expert has identified three key areas landlords can address to ensure they get off to the best possible start with a new tenant and their property manager.

With rents still on the rise around the country, property investors could be excused for thinking the rental income will look after itself.

But with mortgage repayments devouring much, if not all, of that extra rental income, it can pay dividends to enlist a property manager and adhere to some essential tips to maximise rental returns from the outset of the investment.

Kirsty Pilcher, Head of Department – Property Management, aussieproperty.com, has identified three vital components to ensure a rental property is best placed to attract the right tenants, retain its value and capitalise on record low vacancy rates and a tight rental market.

Set the standard early

Presenting your property to the highest standard before a tenant has been secured has many benefits.

Your advertising photos will look fabulous and you are more likely to attract a higher quality tenant who is looking for a well-presented home.

However, something not often considered by an owner is that when a property is handed over at the start of a tenancy, if this property has been professionally cleaned and the gardens recently attended to, it sets the standard for all of the following routine inspections and ultimately the final inspection.

The tenants must continue to present the property to the same standard and return the property in the same condition when the tenancy comes to an end.

If the tenant chooses not to maintain the same standard throughout the tenancy, this is obvious and can be addressed by your property manager, usually at the tenants’ expense.

Prepare a maintenance budget

Maintenance issues at your investment property can be costly and may come at a bad time.

Under the Residential Tenancy Act WA, for example, reported maintenance must be attended to within certain timelines. An owner is obligated to meet these timeframes.

Having a maintenance budget allows your property manager to organise repairs in a timely manner and also service appliances regularly to help avoid emergency maintenance situations arising.

Have proof of ownership ready for your property manager

Under the Residential Tenancy Act your property manager must confirm you are the owner of the property being rented out.

We cannot begin the process of managing your property without this.

The best way to prove ownership is to provide a copy of your Certificate of Title.

Your property manager can order a new copy of this, however, there are costs involved.

To avoid that cost and any delays with getting your property advertised, have your copy ready to pass on at the time of signing your Management Authority.

In addition to these property management tips, property investors looking to buy a rental property should also be aware of these top three rental market factors when trying to pinpoint that successful investment, as well as the need to have adequate insurance coverage.

Article Q&A

What should landlords do before they rent out their property?

A leading property manager has identified three key areas that will ensure a new rental tenancy goes as smoothly as possible, including tips on maintenance, property presentation and contractual requirements.

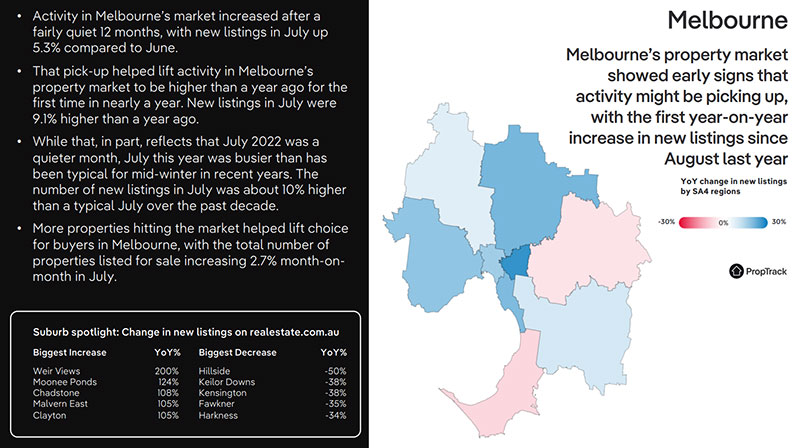

Melbourne’s gradually improving property is teasing real estate investors, with some booming suburbs highlighting the potential upside.

Melbourne property values and land sales are on the up but local experts have mixed opinions on whether to call it the beginning of a sustained recovery.

Listings are on the rise too, easing price pressure but indicating to sellers that previously reluctant sellers are making a move for the spring selling season.

Price boosts are being seen across a range of Melbourne suburbs, with PropTrack data commissioned by APIMagazine revealing the the largest quarter-on-quarter change for house and unit growth value.

Leading the charge for houses, Riddells Creek is up 13 per cent from $948,000 last quarter to $1,070,000, and Olinda is up 12 per cent from $1,010,000 to $1,135,000.

Days on the market vary between 17 and 20.5 for houses, and 23 to 27 for units, with Bayswater North having the shortest days on the market for houses at 17, and Ringwood East the shortest for units, at 23 days.

Melbourne property turning corner

Steve Janes, Real Estate Agent, aussieproperty.com, acknowledges the Melbourne market’s wheel is finally turning.

“Transactions are happening, people are being realistic, and I think three to six months ago there was probably more uncertainty and there seems to be a bit more confidence on both sides of the transaction now.

Steve Janes, Real Estate Agent, aussieproperty.com

“My feeling is the number of buyers in the marketplace has reduced but even more so the number of sellers has also reduced.

The Real Estate Institute of Victoria (REIV)’s latest auction results reported a clearance rate of 78 per cent, up from 71 per cent in the previous week, and from 537 auctions reported.

REIV’s total volume from 316 properties sold was $488 million and an additional $99 million came from 127 private sales.

Melbourne was the only city to see a decline in week-on-week auction activity.

Top five Melbourne suburbs for listings

Listings are up 200 per cent in the Weir Views, which is one of top five Melbourne suburbs identified in REA Group’s July PropTrack Report, for their year-on-year increase, and includes Moonee Ponds up 124 per cent, Chadstone, 108, and Malvern East and Clayton both up 105 per cent.

“Activity is likely to continue increasing over the next few months as we head into the spring selling season, with activity likely to peak over October and November,” Angus Moore, Senior Economist and Report Author, PropTrack, said.

Housing developments are largely the cause, but the report’s overall figures show Melbourne has bucked a nationwide trend in the usually quiet month of July by increasing its listings 5.2 per cent. Year-on-year, listings are up 9.1 per cent, however, the PropTrack report stresses the figures reflect a low base starting point from an even slower July 2022.

Source: PropTrack

Victorian residential development sales company, RPM Group, has seen a rise in land sales for the first time in 18 months, documented in its just released Greenfield Market Report Q2 2023.

“In a normal market, we do around 1,600 lots per month and we were around the 500 lots per month through November, December, January, then it got back up to 650 and we’re now back up, for two months in row, at 750 lot sales, and it feels like we’ve reached the trough because it’s very similar numbers to our last trough, which is back in the middle of 2019,” Luke Kelly, Managing Director, RPM National, told API Magazine.

Luke Kelly, Managing Director, RPM National

“These all look like good signs, and we now need to not have interest rates go up further because there are some good genuine deals in our space at the moment for land developers and for builders, and while they’ve been playing catch up with construction in the last couple of years, where timeframes for delivering a block back then blew out to 18 to 24 months, that’s now come back to within nine to 12 months,” Mr Kelly said.

The report illustrates the growth in the Northern Growth Corridor of Melbourne, in areas like Whittlesea and the City of Hume, that takes in established suburbs of Broadmeadows, Tullamarine and Gladstone Park in the south, the developing residential suburbs of Craigieburn, Greenvale, Mickleham, Kalkallo and Roxburgh Park in the north-east and the Sunbury township in the north-west.

They have had the highest proportion of growth of all corridors in a decade at 35 per cent, where owner-occupiers made up 73 per cent of buyers with just over half being first home buyers.

Harley Toyle, Sales Consultant and Auctioneer, Buxton Stonnington

While the city area of Stonnington East gets a mention, Harley Toyle, Sales Consultant and Auctioneer, Buxton Real Estate Group – Stonnington, told APIMagazine the neighbouring inner circle suburbs of South Yarra, Windsor, Prahran are three core areas where stock levels are very low.

“From a housing perspective, stock levels are very extremely strained, so there is just not a lot on the marketplace; there are still a lot of buyers out there, there’s still really good sentiment, but there just isn’t a lot on the market, which is bolstering prices,” Mr Toyle said.

Article Q&A

Which are the best performing Melbourne suburbs for property price growth?

For houses, the best performing suburbs for capital growth in the past three months have been Riddells Creek, up 13 per cent to $1,070,000, and Olinda, up 12 per cent to $1,135,000. For units, Malvern and Templestowe Lower but shot up by 12 per cent.

Are property prices rising in Melbourne?

Melbourne property values and land sales are on the up but local experts have mixed opinions on whether to call it the beginnings of recovery.

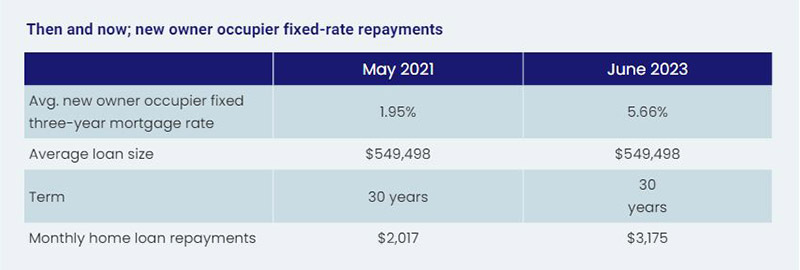

With the mortgage cliff around the halfway point of its gradual transition from low fixed to high variable rate loans, is a looming disaster unfolding or are borrowers proving to be more resilient than expected?

It’s late August and the midway point of what was dubbed the mortgage cliff.

This so-called cliff was named to denote the lemming-like fate that supposedly awaited all who had to move from super low fixed term loans secured from mid-2020 to mid-2022 to loans up to triple that interest rate.

While its progression is far from complete, and much of the impact of this mass switch may still be yet to play out in full, the doomsday scenarios have not eventuated at this stage at least.

There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings over the past few weeks.

But overall, the risk of arrears and default remains contained within Australia’s large mortgage market and a level of resilience demonstrated amid tight labour market conditions.

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season.

While homeowners are, in broad statistical terms at least, not selling up en masse, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

The mortgage cliff was all media hype. – Helen Avis, Director of Finance, Specialist Mortgage

The number of Aussie home loan holders refinancing soared 13.8 per cent in the financial year just completed, while those signing new mortgages fell 20.6 per cent, new research from PEXA shows.

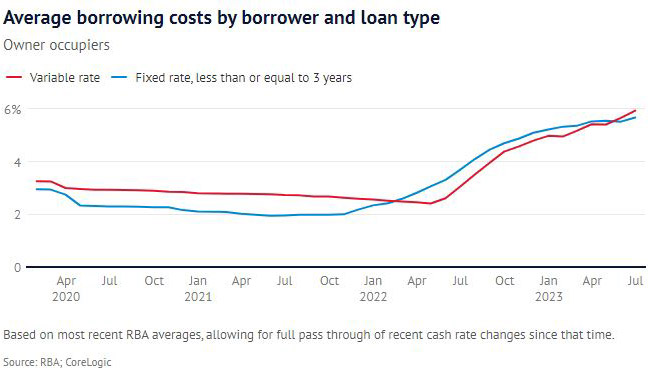

That comes as mortgage holders contend with a transition from interest rates on a loan of around 1.9 to 2.5 per cent leaping to between 6 and 7 per cent.

In terms of what that means to a household’s budget, the repayment on a $750,000 mortgage set at 2 per cent would soar from $3,180 a month to $4,830 a month – an increase of more than 50 per cent overnight, assuming a new rate of 6 per cent.

Yet it seems official data on mortgage stress has not seen a blow out in arrears amid the expiry of low fixed-term loans.

Portion of outstanding loans in arrears

Eliza Owen, Head of Residential Research Australia, said as home values rise, the risk of default also remains low.

“As what is likely to be the last of the RBA’s rate hikes is passed through to households with a mortgage, there may be a mild deterioration in housing market conditions if new listings decisions continue to rise.

“The good news for mortgage holders is that this period of economic slowdown will also take the RBA closer to its long-term inflation target, which could be the impetus for a reduction in the cash rate in the second half of 2024, as predicted by most major banks.”

Whether there is another 0.25 per cent increase in the official cash rate by the RBA is an even money bet. But the governor, Philip Lowe, used the just-released RBA Board Minutes for August to acknowledge the mortgage cliff was a consideration in their decision-making process around interest rates.

“Members noted that banks had continued passing increases in the cash rate through to their customers, and that outstanding mortgage rates and scheduled mortgage payments were set to increase further as a high share of fixed-rate loans roll onto higher rates through the rest of 2023.

“Scheduled mortgage payments as a share of household disposable income increased to 9.4 per cent in the June quarter, around its historical peak.

“Voluntary principal payments into borrowers’ offset and redraw accounts declined in the June quarter (while) net flows into these accounts had declined to be noticeably lower than the pre-pandemic average, consistent with pressures on disposable incomes.”

To be more concise, borrowers are hurting.

Finding more than $1,000 a month for mortgage repayments isn’t easy for everyone.

Climbing or falling from the mortgage cliff?

Industry sources are divided on just how severe the implications of the mortgage cliff’s continued unfolding will become. Some argued it was driven by an excitable media while others declare it’s downward spiral with no imminent escape route.

In the former camp, Helen Avis, Director of Finance at Specialist Mortgage, said “the mortgage cliff was all media hype.”

“I cannot see rates rising too much further, and if that is the case then we should not see much more of an adjustment from where we are at now.

“I am not surprised with the lack of delinquencies, with the still relatively strong property market and borrowers able to handle the increases.

“That said some borrowers have been affected and are struggling but the vast majority seem to be coping.

“I know some first home owners who have rented their property and gone back to live with parents, capitalising on the acutely tight rental market to offset the stress of higher mortgage repayments.”

Joe White, President, Real Estate Institute of Western Australia (REIWA), said we are well into 2023 and we have not seen the apocalypse we were told was coming.

“While there have been constant predictions of a flood of forced sales, REIWA data does not yet show an increase in properties advertised as mortgagee sales or mortgagee in possession.

“There is no denying 12 interest rate increases have had an impact on households, but it is disingenuous to underestimate a homeowner’s capacity and willingness to adjust their spending habits.

“Many homeowners on fixed rate loans have prepared for the dreaded mortgage cliff.

“They have paid extra onto their mortgage to be ahead with their repayments, have created a savings buffer or have refinanced.”

API Magazine’s recently released Property Sentiment Report found that the percentage of respondents defining their situation as being in mortgage or rental stress was easing.

While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Mark Bouris, Executive Chairman, Yellow Brick Home Loans, however, was far less optimistic than others, reporting that the consequences of the interest rate hikes won’t be fully laid to bear until Christmas this year, as more and more home loans move from cheap fixed rates to high variable rates.

“Expect families to be forced to sell their homes, many to property investors and foreign buyers, and end up in the already-crowded rental market that is driving up inflation.

“Otherwise, families will be forced to cut back their spending on everything from holidays to food to recreational activities and school fees – the list goes on.

“This will hurt the small businesses that rely on consumer spending to pay their bills, which are also rising.

“It’s a vicious cycle, and there’s no clear way out.”

There has been a sharp spike in landlord exits from the property market across Australia.

Victoria is the worst-hit state, with the latest PropTrack figures revealing 30.1 per cent of sales were properties that had been listed for rent since they were purchased.

That’s up from 24.7 per cent in July 2022, and 16.9 per cent in July 2019, before the pandemic. New South Wales followed at 28 per cent, which like Victoria, was also the state’s highest share of investment home sales since late 2018. Queensland was third with 27.15 per cent of sales in July being rental properties.

Regardless of which side of the fence you sit on in terms of the mortgage cliff’s ultimate impact, the rest of the year promises to offer compelling viewing of the economy, housing market, and the financial viability of renters, home owners and investors alike.

Article Q&A

What is a mortgage cliff?

The mortgage cliff refers to the sudden large increase in repayments mortgage holders on fixed rate loans will face when their term ends and their loans revert to variable, and the subsequent effect this will have on the property market.

What has been the impact of the mortgage cliff?

While its progression is far from complete, the doomsday scenarios of the mortgage cliff have not eventuated at this stage at least. There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings.

Will property prices fall because of the mortgage cliff?

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season. While homeowners are, in broad statistical terms at least, not selling up en masse because of the mortgage cliff, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

Would a ban on foreign property investment, as has been implemented in Canada, improve housing affordability in Australia?

In an attempt to rein in property prices and reduce the number of homes sitting vacant, Canada this month took the major step of banning foreigners from buying residential property.

Given the property market similarities between Canada and Australia in terms of price, supply, affordability and even political and social culture, it raises the question of whether Australia’s still expensive real estate would benefit from such a prohibition.

The Canadian ban, a two-year measure for now, was first proposed by Prime Minister Justin Trudeau when property prices were soaring but as in Australia and for mostly the same reasons, prices have recently eased.

There is a widely held perception in Australia that foreigners drive up property prices and make life difficult for first home buyers.

A survey found a clear majority of Australians (82 per cent) felt foreign buyers from China pushed up Australian housing prices. Around seven in 10 Australians (69 per cent) also said Chinese investors in Australian real estate had made it difficult for first home buyers in Australia to enter the market.

But the reality is that foreign buyers only account for around 1 per cent of total transactions in the Aussie property market and 4.6 per cent of new development purchases, so their impact is limited.

First home buyers are probably immune to the impact of foreign buyers too, with overseas investors on average spending $1.5 million on their property purchase.

Foreigners living overseas are only allowed to buy new or off-the-plan properties for investment, which also limits their impact on the price of established properties.

Ban could raise Australia’s property profile

Real Estate Buyers Agents Association (REBAA) president Cate Bakos said Canada’s ban could generate more interest from international buyers in Australian property but said foreigners already had to overcome significant tax and approvals hurdles.

“There could indeed be some implications if Australia was to take this same stance as Canada and it’s important to note some of the various reasons why foreign purchasers make the decision to buy in Australia,” Ms Bakos said.

“Not all foreign buyers are doing so purely for investment reasons.

“Some are parents sourcing properties for student children, while others include parents attempting to stay part-time in a carer capacity for student children.

“Importantly, our country limits foreign investment activity in residential, agricultural and commercial land and foreign buyers are subject to Foreign Investment Review Board (FIRB) approval.

“The limitations are reasonably strict and most foreign buyers are only able to purchase brand new property as opposed to established.

“Our current new building rate is limited as it is, so I’d argue it’s quite difficult for foreign investors to target Australian property at present.”

New dwellings represented 68.6 per cent of international buyer purchases, followed by 18 per cent for vacant land, and 13.4 per cent for established dwellings in 2020‑21.

Head of Research of buyer’s agency InvestorKit, Arjun Paliwal, said the current rules meant foreign buyers were supporting housing supply creation, given only 13.4 per cent of a very small base of transactions go on to compete in the established market.

“In Australia, we already make foreign buying of property difficult through regulations and expensive through surcharges and taxes,” he said.

“Australia following along with other countries on a ban on foreign property buyers would be a decision that is misguided and one that would not make any meaningful difference to housing affordability.”

Ms Bakos added that the two most expensive taxes and duties are already a disincentive to many foreign buyers.

“Land stamp duty rates are significantly higher for foreign buyers as are land tax rates.

“While they may be eye-watering for some, for those who can afford the taxes and duties, our tax revenues are tolerated.”

Canada’s ban could actually raise the profile of Australia among foreign investors.

“Australia can expect to see an increase in buyer interest as a result of Canada’s decision.

“Our two countries share some parallels and it’s fair to assume that Australia will be considered an alternative option.”

To alleviate the problem of foreign-owned homes sitting empty, Victoria’s state government has introduced a vacancy tax for foreign owners not utilising their homes. This annual tax is set at 1 per cent of the capital improved value (CIV) of taxable land (or $10,000 on a million-dollar home).

High taxes an investment deterrent

Even allowing for the Canadian ban, there’s no guarantee Australia will be best placed to attract foreign investment in residential property.

Real estate agent with aussieproperty.com, Steve Janes, said foreign investment in Australia was used as an economic stimulus in during the previous GFC downturn.

“The construction boom, particularly high-rise development and house and land packages, of the past decade targeted foreign investment and largely insulated us from global downturns and later boosted our economies,” he said.

“Over the last two to three years, however, foreign investment has already been deflected with increases to foreign buyer stamp duty and inflated FIRB costs to the point that today Australia is already far less attractive for foreign investors, many of whom will most likely continue to divest and seek higher returns elsewhere.”

China opens investment door

Canada’s ban came just days before China threw open its borders and international real estate investment is expected to be invigorated as a result.

Top countries for Chinese property buyers

1

Australia

2

United States

3

Canada

4

Japan

5

Thailand

6

United Kingdom

7

Malaysia

8

United Arab Emirates

9

Vietnam

10

South Korea

Source: Juwai IQI (as of December 2022)

Kashif Ansari, CEO, Juwai IQI, said Chinese international property investment dropped by 50 per cent to 60 per cent during the pandemic but is already beginning to recover from its pandemic lows.

This will be the first opportunity in three years for most Chinese to visit overseas real estate markets,” he said.

“China has gone from virtually sealed off to nearly wide open within just a couple of weeks, and travellers’ priorities include visiting family and friends, studying abroad, business, tourism and property investment.”

“We expect Chinese outbound travel and accompanying property investment to increase rapidly in January from its current very low level.

“We can’t bounce back to 2019 levels all at once but outbound travel from China will snowball and may reach 2019 levels by mid-2024.”

Article Q&A

Can foreigners buy residential property in Australia?

Foreigners living overseas are only allowed to buy new or off-the-plan properties for investment and are also subjected to higher land taxes and other financial impositions.

What proportion of property sales in Australia are to international buyers?

Foreign buyers only account for 4.6 per cent of the Aussie property market transactions. Of these, new dwellings represented 68.6 per cent of international buyer purchases, followed by 18 per cent for vacant land, and 13.4 per cent for established dwellings in 2020-21.

SMATS Group, who provide Australian taxation, finance and property investment services, have provided their top five tips to ensure property investors and buyers can navigate the tax maze.

Australia’s tax regime is regarded as one the most complex in the world, where working from home or renting out a room can generate more recordkeeping than a vinyl music collector.

But if Australia is record holder for generating tax minutiae, it also necessitates the need for a strategy worthy of a world record marathon runner. It’ll probably take more than the record-setting two hours, one minute and 39 seconds achieved by Kenyan Eliud Kipchoge in the Berlin Marathon, but some attention to detail will likely result in a run of savings.

SMATS Group, who provide Australian taxation, finance and property investment services, have provided API Magazine with their top five tips to ensure property investors and buyers can go for gold, both literally and metaphorically.

Capital gains tax (CGT) implications on claiming occupancy expenses on your current residential address

Occupancy expenses include things like your rent or mortgage interest, property insurance, land taxes or rates. You can only claim occupancy expenses if you can show:

it was necessary for you to work from home because your employer doesn’t provide you with an alternative place from which to work

the area of your home that you use for work is exclusively or almost exclusively used for work purposes.

When you claim a deduction for occupancy expenses, the capital gains exemption that applies to your main residence when it is sold (the exemption that makes the sale tax-free) is partially reduced. The reduction is based on the percentage of the floor area of your home that is considered a place of business.

This may result in a tax consequence upon its sale. Due to this, it’s not usually recommended that you claim this method if you own your home.

Obtaining a depreciation report

We recommend obtaining a depreciation report (or schedule), if the property was built after September 1985 (or had major renovations performed after 1991).

Obtaining a depreciation schedule allows a tax deduction claim for the building costs along with any new fixtures that have been installed. The depreciation report only needs to be ordered once for the life of the property but normally provides an annual tax deduction of many thousands of dollars.

Note that the tax deduction can be claimed against an investment (rental) property on the year it was incurred, however, if the property was not genuinely available for rent, then the depreciation not claimed in the tax year in question will form part of your reduced cost base.

Capital gains tax discount for individuals who were foreign-tax residents during the time they owned the property

Up to 8 May 2012, any resident or foreign-tax resident individuals that held investment properties for at least 12 months before selling the asset were qualified for the 50 per cent CGT discount.

The 50 per cent CGT discount is no longer available for foreign-tax residents from 9 May 2012.

If an individual sells an investment property after 8 May 2012 while a foreign tax resident, and the property is expected to generate capital gains upon its sale, then it is recommended you obtain a market valuation as of 8 May 2012.

This will allow the 50 per cent CGT discount to be applied from the date the property was purchased to 8 May 2012.

If a market valuation is not obtained for an investment property as of 8 May 2012, the CGT discount percentage will then be recalculated, not taking into account the 50 per cent CGT discount for gains accumulated up to 8 May 2012.

Additionally, if the market value of the investment property as of 8 May 2012 is equal to or higher than the actual selling price, then the foreign-tax individual will be entitled to the full 50 per cent CGT discount.

The temporary absence rule

When an investment property was a taxpayer’s main residence for only part of the ownership period, then a partial main residence exemption is applied upon its sale.

In this situation, the ‘temporary absence rule’ allows a taxpayer to choose to continue to treat the dwelling as their main residence for all or part of the period they did not reside in it.

The temporary absence rule applies for the following:

The taxpayer can treat the dwelling as their main residence indefinitely if the property is not used for income producing purposes after the taxpayer moves out; or

The property can be treated as the taxpayer’s main residence for a maximum period of six years while it is used for income-producing purposes during a single period of absence after the taxpayer moves out (e.g., it is rented out).

Negative gearing, borrowing, or leveraging

Your investment property is said to be geared when a loan is taken out to purchase a rental property.

It is common for an Australian residential property to incur running expenses greater than the rental income received. If this is the case, a negative gearing loss arises.

The taxable loss generated from the negative gearing can be offset against other assessable income, including employment income, therefore providing tax savings.

These negative gearing losses are available to accrue forward (over multiple tax years) and can be offset against Australian taxable income in the future, including:

Australian business income

employment income

capital gains.

For Australian tax residents, if you expect your rental property to generate a loss in the financial year, you can contact the tax office to reduce the amount of tax withheld from your salary (known as PAYG Withholding Variation), allowing for a cash flow boost.

Disclaimer: All information provided is of a general nature only and does not take into account your personal financial circumstances or objectives. Before making a decision on the basis of this material, you need to consider, with or without the assistance of a financial adviser, whether the material is appropriate in light of your individual needs and circumstances. This information does not constitute a recommendation to invest in or take out any of the products or services.

Since the emergence of COVID-19, Australia has become a premier global destination for our enviable lifestyle, stable political system, world class health care and affordable real estate. Foreign buyer activity has increased as much as 22% for some states!

Send us your questions via email to smats@smats.net

Find Us: https://www.smats.net/

Find Us: https://www.aussieproperty.com/

Liability limited by a scheme approved under Professional Standards Legislation. Australasian Taxation Services Pty Ltd (ATS) – ABN 60 068 961 400 | Registered Australian Tax Agent 62364000.

COPYRIGHT: Except as permitted by the copyright law applicable to you, you may not reproduce or communicate any of the content on this video, without the permission of the owner.

DISCLAIMER: The information in this video does not take into account your individual objectives, financial situation or needs. We recommend that you obtain financial, legal and taxation advice before making any decision.